Shiny Object or Actual Transformation?

Welcome to the 46th edition of The LogTech Letter, a weekly look at the impact technology is having on the world of global and domestic logistics. Last week, guest Jonah McIntire, CEO of TNX Logistics, discussed the lack of winner-take-all scenarios in trucking technology. This week, I’m delving into the connection between specific industry sectors and their respective appetites for logistics innovation.

As a reminder, this is the place to turn on Fridays for quick reflection on a dynamic, software category, or specific company that’s on my mind. You’ll also find a collection of links to stories, videos and podcasts from me, my colleagues at the Journal of Commerce, and other analysis I find interesting.

For those that don’t know me, I’m Eric Johnson, senior technology editor at the Journal of Commerce and JOC.com. I can be reached at eric.johnson@ihsmarkit.com or on Twitter at @LogTechEric.

One of the perks of my job is I get to have off-the-record chats with executives at some of the most impactful companies in the logistics industry. I’ve found that software executives who have been through a few cycles of logistics technology development have a pretty well-rounded view of the world.

It was one such conversation this week that had me thinking about the extent to which international shippers are actually innovating through investment in technology. More to the point, is there a connection between the type of shipper and its willingness to invest in transformative technology?

There’s always a tendency to generalize when it comes to software adoption, but as I’ve written about before, the industry is not monolithic, and that is especially true when it comes to shippers. Even shippers in the same sector that are roughly similar in size and selling to similar markets can have drastically different views about logistics management and outsourcing of functions. But it’s especially true that shippers in different verticals are likely to be driven by entirely different incentive structures.

As the software executive I spoke with put it, the need to innovate in logistics is often driven by the pace of ultimate consumer innovation. Fast fashion and high-tech brands have absurdly fast product cycles, and their supply chains (including the logistics components) need to support that reality. A CPG shipper that’s been selling the same toothpaste SKU for 10 years doesn’t operate under the same constraints.

In some respects, the type of goods a shipper makes or imports is a window into that how much innovation that company is willing to introduce into its supply chain systems. But…there’s an interesting aspect to this dynamic: CPG companies and other companies that aren’t necessarily compelled to innovate on product relentlessly (ie alcoholic beverage producers) have publicly been some of the most innovative shippers. Companies like AB Inbev and P&G and Unilever are working with an inordinate amount of early-stage logistics technology companies. The question is this: what is for show and what is actually transforming the business from the inside out.

I found this mini-thread from Dynamo Ventures Founding Partner Santosh Sankar illustrative.

Let’s be clear: some early stage technology providers are definitely making inroads with enterprise global shippers. But, just as that is true, if a large CPG company is doing pilots with 20 different startups, not all of those pilots will turn into long-term commercial relationships, much less transformative innovation.

As I described in this JOC article in March, there are misaligned incentives when it comes to large shippers using startups to transform their logistics functions. Startups generally need to focus on hyper-specific solutions to narrow problems in order to get traction and investment from venture capital firms. And large shippers, as the software executive emphasized to me this week, are simply incapable of overhauling their existing stack in one go, much willing to do so. The result is that large shippers with longer product lifecycles use startups to tinker on the periphery in the hopes that one or two can drive actual change. But even that comes gradually.

What’s interesting is that the reputational leverage in these relationships has sort of flipped in recent times. Whereas a few years ago a large shipper with a solid brand and a static set of products might have avoided been linked to high-risk, early-stage startups, now they are keen to be associated with the perception of innovation those startups produce.

The dynamic is different for those companies with shorter product lifecycles, and here is where startups are likely to make hay. There is, in fact, a need for these companies to be adaptive to changing consumer behavior, rising customer expectations around speed of delivery, and wildly fluctuating freight supply cycles. In those industries, companies sit still at their peril. And so, you can generalize that companies with lightning fast product cycles are going to gravitate more meaningfully to early-stage logistics technology companies, while those with more static product sets will use startups as more of an outward signal that they are willing to embrace innovation.

But the ultimate proof is in who adopts and pays for what type of system. Large established shippers still mostly rely on name-brand, established logistics planning, procurement, and management suites. That’s the norm, and use of an early-stage software product is the anomaly. Of course, that will change over time. A few of today’s upstarts will become the established brands of tomorrow, and the companies with faster product turnover will live at the bleeding edge of driving that change. And the cycle will repeat.

Broadly, this is to say that the pace of logistics innovation and the role of early-stage tech providers in that movement is highly dependent on which type of shipper you are looking at. As much as we like to think that things like COVID-19 and the current global shipping capacity crisis might herald a change across all industries, there is decades of software infrastructure to be dismantled. And that dismantling will not happen at an even pace across all industries.

🚨 TPMTech is coming to Long Beach Feb. 24-25!

I’ve lost track of the number of times I’ve been asked if the JOC is holding our LogTech conference in Las Vegas this year. While the answer to that is no (as far as it being in-person), the good news is we’re holding our first ever TPMTech Conference in advance of TPM22 next year. You can think of TPMTech as a sort of hybrid of LogTech and El Dorado, the concurrent tech event we never got a chance to hold in Long Beach during TPM20 due the onset of COVID-19. The event is a standalone event, but you can of course register for both TPMTech and TPM22 in a package at a reduced rate. My hope is that there is lots of crossover between the two events. TPMTech will be the place to discuss what’s on the horizon, but we’re not ignoring technology on the main TPM22 program agenda - sessions there will focus on existing market challenges and the role technology plays in managing them. More news to come on TPMTech in the coming weeks, including how to register, hotel options, programming, and of course demos and networking. Can’t contain my excitement about this.

Here’s a roundup of pieces on JOC.com the past week from my colleagues and myself (note: there is a paywall):

In the world of logistics technology, doesn’t get much buzzier than the two companies that have raised the most venture capital integrating with one another. Flexport has been a customer of Convoy since 2018, but the two companies have set about making their relationship less transactional. I’m sure some hardened eyes will roll, but let’s be clear. These two companies have some percentage of a collective $2 billion in capital to play around with, so ignore their under-the-hood product development at your peril. This partnership is also likely to instigate some rumors around acquisition, which is natural, but I’ve not heard anything concrete yet.

I spoke with the authors of this study on how the pandemic might affect shippers’ decisions around sourcing globally or locally. For me, the big issue is how shippers balance supply chain efficiency versus resiliency. And technology will surely play a role in determining that balance.

Not technology-related, but since spiking ocean rates have hit the mainstream, thought I’d link to my colleague Greg Knowler reporting on Moody’s expectations that freight rates will stay high well into 2022.

And here are some recent discussions, reports, and analysis I found interesting:

It’s always instructive to read Rob Garrison’s blogs at Mercado, and this one on the current ocean capacity crisis is obviously very topical.

Sustainability is legitimately becoming a decision-making factor in supply chains. Here’s a worthwhile blog from Pierre Garreau of the carbon calculation technology provider SeaRoutes.

One of my favorite Twitter follows over the years has been Hanna Norberg, and I was super pumped to see her formally launch the Trade Experettes, which is undoubtedly set to become the most informed network of trade professionals globally (if it isn’t already). Trade has always been an industry that’s historically run counter to logistics in that the vast preponderance of practitioners and executives are women, and this network is a celebration of that collection of talent. If you need any guidance on any trade-related matter, this is the place to turn.

Another digital forwarder, this one in Latam, gets funding. I talked to Max Casal at Nowports a long time ago, so exciting to see his vision get backed by some pretty heavy hitter VCs.

Interesting white paper from e-commerce shipping startups Shippo and ShipBob (both of which recently reached 🦄 status).

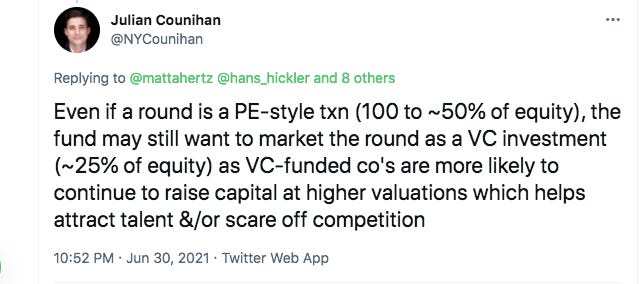

Speaking of e-commerce and VC funding, wanted to point out this tweet from Julian Counihan on an interesting wrinkle in the debate over whether a funding event is VC or PE. Thanks to Matthew Hertz for asking the question.

Some upcoming events I’ll be involved in:

I’m joining Sarah Barnes-Humphrey on her show 10 am EST July 6, where we’ll be talking about some news coming in August – I’m launching a new show on her network Aug. 6 called LogTech Live. More details to come, but I’m obviously super excited about this and big thanks to Sarah for the opportunity!

I recorded a webcast with SupplyStack, BMW and Wallenius Wilhelmsen earlier this week, and there were some fantastic insights about the role of digitization, TMS, real-time visibility and automation in vehicle logistics. Much of the perspective is broadly applicable to other industries, especially as BMW’s Hans Dormann Osuna describes the logistics challenges of satisfying changing customer demands. Definitely encourage you to check out the recording.

Thanks to Nieves Perez for talking to me about the current shipping capacity and freight rate situation. This one’s for my Spanish-speaking followers!

I’m delighted to be joining Eytan Buchman of Freightos at 8 am EST July 14 to celebrate the one-year anniversary of his Future of Freight series. I was honored to be the very first guest and pumped to discuss a range of really important topics with Eytan, who is dangerously close to being a journalist himself with the incisive questions he asks.

Disclaimer: This newsletter is in no way affiliated with The Journal of Commerce or IHS Markit, and any opinions are mine only.