A Cold Dose of Low Margin Reality

Welcome to the 19th edition of The LogTech Letter, a weekly look at a particular aspect of the impact technology is having on the world of global and domestic logistics. Last week, I touched on the differences between on-demand models that tap into latent capacity in the consumer space and those in the logistics industry. This week, I’m getting to the heart of a pretty important issue: the intrinsically low-margin nature of global logistics and what that means to the viability of LogTech software companies.

As a reminder, this is the place to turn on Fridays for quick reflection on a dynamic, software category, or specific company that’s on my mind. You’ll also find a collection of links to stories, videos and podcasts from me, my colleagues at the Journal of Commerce, and other analysis I find interesting.

For those that don’t know me, I’m Eric Johnson, senior technology editor at the Journal of Commerce and JOC.com. I can be reached at eric.johnson@ihsmarkit.com or on Twitter at @LogTechEric.

What’s the average profit margin in forwarding? How about freight brokerage? How about for asset-based companies, like container lines and trucking companies? We can quibble about which of those sectors is more attractive, and which specific operators are better at carving out an above-average margin. But the broader issue is that everything in logistics is relatively low margin when you compare it to other industries. And that matters when we think about whether there’s an opening for a software-as-a-service (SaaS) company to transform the logistics industry and, by doing so, get multi-billion dollar valuations..

I’ve argued in previous editions of this newsletter that the size of the logistics industry (or in investing parlance, the total addressable market) is overstated, and also that the industry is so intrinsically fragmented and regionalized that it will be hard for a single company to create a dominant share in SaaS like, say, Salesforce has in CRM or Oracle and SAP have in ERP.

This is important context for the hard reality of the low-margin discussion. Without a fundamental reconstruction of the entire industry - which, frankly, is unlikely - it’s hard to see how margins in logistics expand to the point where a flood of investors back startups in freight transportation and warehousing as they have in other industries. It may seem like logistics is a hot market based on the slew of funding rounds this year, but there’s an order of magnitude issue at play here.

E-commerce logistics SaaS companies get near-$300 million private equity rounds. Food delivery apps IPO at $100 per share and $70 billion valuations and then immediately trade at double that number (rolling my eyes aggressively as I type that sentence). Meanwhile, a logistics SaaS company gets a $50 million Series B and the industry’s tongues wag as they shake their heads at all the cash spoiling the market.

Don’t let the $1.3 billion Flexport and $665 million Flexport and Convoy have respectively raised obscure this point: those were operators able to show revenue immediately, and then able to grow that revenue at the speed at which makes VCs take notice. But they are not - yet, at least - SaaS companies.

Let me put a finer point on this. A logistics software founder and I had an interesting discussion a couple weeks back. He asked rhetorically “how many $1 billion logistics SaaS companies will there be in 10 years?” I didn’t have a good answer. Five? Ten? 30? The fact that we didn’t know, and that I was inclined to guess at the lower end of that range, suggests that there is a growth ceiling somewhere. I ran this idea past a couple of VC investors who know the logistics space well, and let’s just say they didn’t vigorously disagree with me.

For many of the reasons I’ve written about in previous editions of this newsletter, it is hard to see an emerging company develop a brand that can capture the imagination of the market the way companies have in other markets. It’s not even the fact that we’re talking B2B and not B2C (since consumers are much easier to wow than cynical B2B buyers). Even casual watchers of the investment space rattle off names like Snowflake and Box and Robinhood and Calm without really having deep domain expertise in those fields. No one mentions logistics software companies like that. Not even Keith Rabois, who knows everything about everything.

Logistics is not a defined market. It covers such a wide range of discrete processes that selling a “this software does it all” product is not really viable. Pain points differ between shippers, 3PLs, carriers, and facility operators. Pain points differ in various regions (even within the same country). Pain points differ even within the same vertical. If I had a dollar for every logistic SaaS provider that tells me these days “I have to be watchful not to build every feature that customers ask me to because it doesn’t scale,” I wouldn’t have to charge you all $5,000 a month for this newsletter.

There are, of course, universalities in the market, but those overlaps are often not at the point of purchase on a software product. By that I mean each potential customer for a product has a unique reason for ultimately investing in software, and those overlapping areas - where multi-tenant, single version software really sings - feel happenstance more than chronic.

Back to the “how many $1 billion logistics SaaS companies will there be in 10 years” question: how many do you think would sell for that much today? How many do you think have a path to sell for that much down the road? How many are truly SaaS, versus a tech-focused operator or some hybrid of brokerage and SaaS?

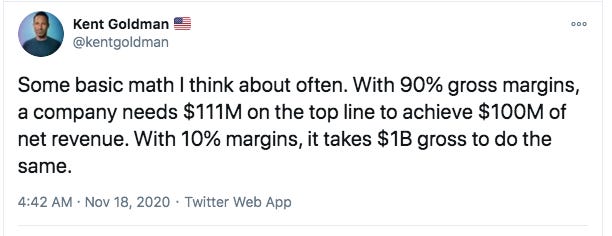

I came across this Tweet in mid-November and I’ve been thinking about it ever since. When I first read it, I chuckled and thought, “water is also wet” and “if I had a million dollars, I’d be a millionaire.” But actually, sometimes you need things to be boiled down to their raw, obvious essence.

Logistics is pretty close to the second scenario and light years from the first. Until that changes, it’s hard to imagine the industry reaching the valuation heights of a Shopify or a DoorDash or a Salesforce because low margin businesses - even massive ones - are just not as attractive to investors as high margin ones. Sorry for stating the obvious.

Here’s a roundup of pieces on JOC.com the past two weeks from my colleagues and myself (note: there is a paywall):

Everyone hates email right? Playing off the news of Salesforce buying Slack for $27 billion (!!!) Sedna publicly announced a previous $10 million funding round last week. That gave it a chance to explain how it plans to help wean enterprises off email. I talked with founder Bill Dobie and a key investor in the company last week.

Documentation automation is a major pain point and opportunity in logistics and trade compliance. And the biggest challenge revolves around how to capture and contextualize commercial invoice data. I spoke with three providers that specialize in that area about the technical challenges and why demand is growing from forwarders.

DCSA releases another standard, this one trained on the elusive interoperable electronic bill of lading. For this to be successful, container lines need to adopt this standard and shippers need to support them in that adoption.

More drop-and-hook news, this time Transfix bringing its own model to the market, which relies purely on algorithms, not equipment. As Jonathan Rojas, vice president of carrier management and operations at Transfix told me, “we don’t see the problem as a lack of trailer capacity, but more about underutilization of existing equipment.”

The TMS provider 3Gtms earlier this year (in the before times) acquired a parcel management provider. The deal was interesting because it not only filled a functionality gap in 3Gtms’ portfolio, it also gave the company the ability to add smaller customers with a dramatically shorter sales cycle. Then COVID-19 hit and e-commerce/parcel movement shot through the roof. Which makes 3Gtms’ integration of invoice auditing software provider OpenEnvoy pretty interesting.

Sustainability technology will be an area to watch in ‘21. SeaRoutes integrating its carbon emission calculation API into CEVA and logistics software providers Portrix and BuyCo is an example of how this might proliferate. CEVA wants to help shippers make carbon footprint a procurement decision maker for its shipper customers (it’s also part of the CMA CGM Group, which is going as big as any container line on decarbonization). Portrix has deep reach within the forwarder community and BuyCo is building that reach in the shipper community.

And here are some recent discussions, reports, and analysis I found interesting:

The DoorDash IPO feels like one of those inflection points in modern history. A company that leveraged the pain of other businesses by helping them barely remain viable, after years of questionable practices and loss-making, is now worth $70 billion? Mmmkay. I loved this blog from mid-’20 about the company’s model.

Andre Simha has a uniquely powerful voice in the container shipping industry and his call to arms on better aligning and making use of port data is worth a read. Incidentally, we’ll have a session at #TPM21 focusing on ports as data hubs.

Not sure I even understand this lengthy blog from Kevin Kwok, but a logistics tech founder passed it along to me and said I should read it. I’ll keep going through it until I properly understand it (which may be in 2050).

From August, Logward CEO Jona Krumland with a humorous look at what’s real and what’s not in logistics digitization.

Still obsessed that Yatra, India’s version of Expedia, has started a digital forwarding business. And curious why I’ve not seen anyone report much on it yet.

Maersk is beta-testing a 4PL business, to go along with its TMS, and small shipper online logistics platform.

🚨 TPM21 registration is live, and so is the agenda. We’ll have two days of #LogTech focused programming Feb 25-26, ahead of the main program, which kicks off March 1. Each week until TPM, I’ll be highlighting a tech-focused session we’ll be hosting.

This week, I’m shining a light on our discussion of how freight procurement is changing due to rate benchmarking, tendering and container allocation software. Guesswork, spreadsheets and MQC/52 approaches aren’t modern ways to handle this huge optimization puzzle. This session will give insights into how to build a better approach, with perspective from Patrik Berglund, CEO of Xeneta, Jonas Krumland, CEO of Logward, and Pieter Kinds, CEO of Freightender.

Disclaimer: This newsletter is in no way affiliated with The Journal of Commerce or IHS Markit, and any opinions are mine only.